Derivatives

In a more specific definition, derivative is a traded financial contract between two or more parties to buy or sold an asset/commodity on an agreed time and price. The future value of the derivative is highly influenced by its underlying asset in the Spot Market.

Financial Derivatives

Derivatives listed in the Exchange are financial derivatives, which derived from financial instruments such as stock, bond, stock index, bond index, currency, interest rate and other financial instruments. Financial derivatives are often used by Investors and Issuers to perform hedging on their portfolios.

Jurisdiction

-

Capital Market Law of the Republic of Indonesia No. 8 year 1995 concerning the Capital Market as amended by Law Number 4 of 2023 concerning Financial Sector Development and Strengthening.

-

Financial Services Authority Regulation Number 32/POJK.04/2020 concerning Securities Derivative Contracts.

-

Financial Services Authority Regulation Number 3/POJK.04/2021 concerning Implementation of Capital Market Activities.

-

Letter of the Head of the Capital Market Supervision Department 2A of the Financial Services Authority Number: S-1245/PM.21/2020 2 dated 1 December 2020 concerning Product Approvals for KBIE LQ45, KBIE IDX30, KBSUN and KBSSUN.

-

Financial Services Authority Letter Number: S-115/PM.02/2024 dated January 30, 2024 concerning Product Approvals for Single Stock Futures.

-

BEI Regulation Number II-E concerning Futures Contract Trading.

Several Derivative products traded at IDX:

Single Stock Futures (SSF)

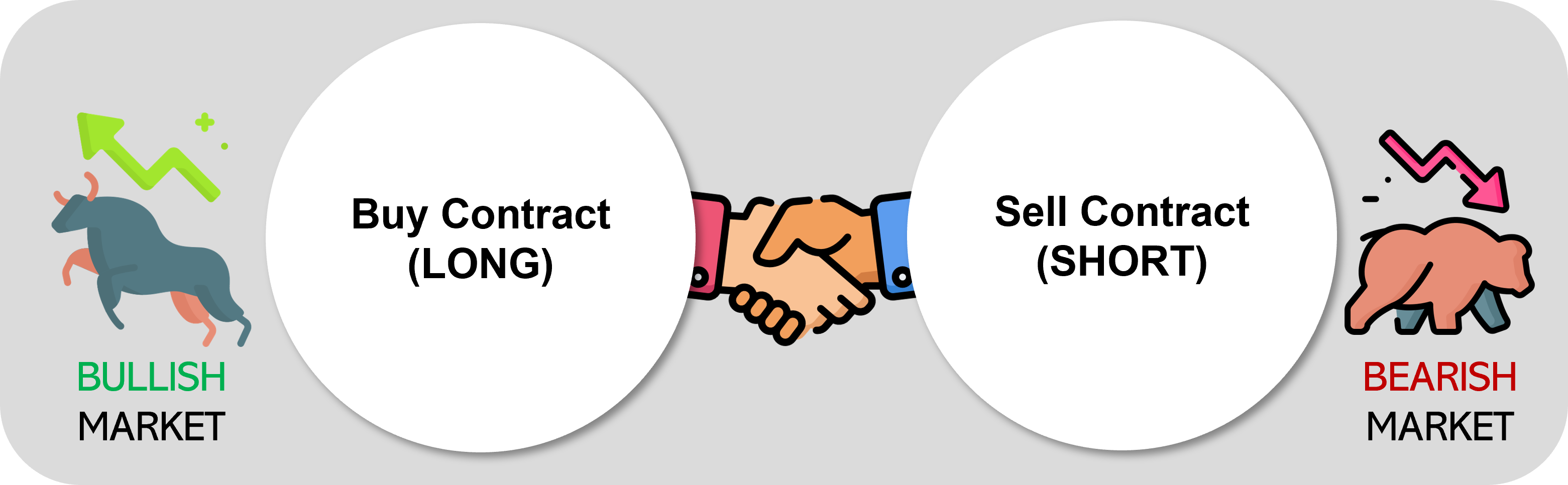

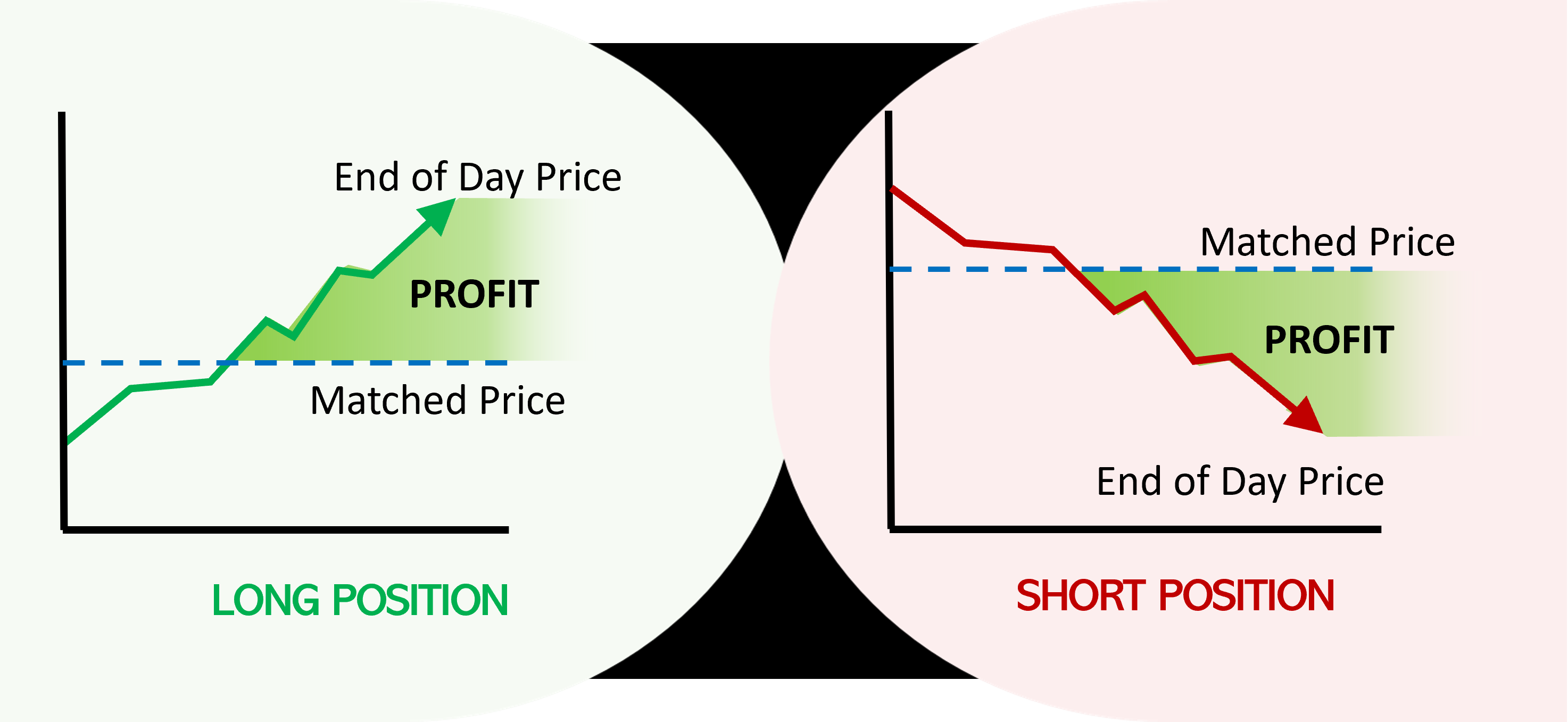

Single Stock Futures (SSF) is an agreement (contract) between two parties to sell or buy shares at a previously agreed price within a predetermined time period.

SSF Contract is divided into 2 (two) types, namely:

- Buy Contract (Long): Agreement to buy shares at a certain price and period.

“LONG” Futures investors will gain profits if the spot price rises since they have locked in a lower purchase price (matched price) than the market price (spot price). - Sell Contract (Short): Agreement to sell shares at a certain price and period.

“SHORT” Futures investors will gain profits if the spot price falls since they have locked in a higher selling price (matched price) than the market price (spot price).

Benefits of Single Stock Futures:

- Earn profit whether the market is going up or down

SSF provides an opportunity for investors to earn profit whether the market is going up or down so that it can be used for both trading and protecting portfolio value. - Smaller capital requirement

SSF allows investors to gain exposure to stock price movement by only paying an initial margin. - Leveraging

SSF allows investors to earn higher profits with smaller capital compared to stock transactions. - Faster profit realization

Transaction settlement is carried out by cash settlement at T+1.

Single Stock Futures Specification:

|

Criteria |

Specification |

|

|

Underlying |

Constituent of LQ45 |

|

|

Multiplier |

100 Shares |

|

|

Contract Size |

Multiplier × Stock Price × Number of Contract |

|

|

Tick Size |

In accordance with the underlying (same with stock) |

|

|

Contract Price |

Price Fraction |

|

|

<Rp200 |

Rp1 |

|

|

Rp200 – Rp500 |

Rp2 |

|

|

Rp500 – Rp2,000 |

Rp5 |

|

|

Rp2,000 – Rp5,000 |

Rp10 |

|

|

>Rp5,000 |

Rp25 |

|

|

Contract Period |

1 Month, 2 Months, 3 Months |

|

|

Initial Margin |

4%* × Stock Price × Number of Contract × Multiplier |

|

|

Auto Rejection |

In accordance with the underlying stock |

|

|

Settlement |

Cash Settlement, T + 1 |

|

More information about SSF

IDX LQ45 Futures

Futures is a contracts to buy or sell an underlying (can be index, stock, bond, etc.) in the future. Index Futures are futures contracts that use stock indices as their underlying. IDX LQ45 Futures is an agreement requiring parties to buy or sell a certain amount of Underlying at a price and within a certain period of time in the future. LQ45 Futures uses the LQ45 index, a well known index that serves as the benchmark of stocks in Indonesian Capital Market, as its underlying. In the fast growing capital market in Indonesia, LQ45 index can be the most effective way in tracking the stocks market of Indonesia in general. Specifications of LQ45 Futures :

| Criteria | Specification |

|---|---|

| Underlying | LQ-45 index |

| Multiplier | IDR 500.000 |

| Tick Size | 0,05 (1bp) |

| Contract Months | 1 Month, 2 Months, 3 Months |

| Min. Initial Margin | 4% X index point X Number of Contract X Multiplier |

| Auto Rejection | 10% |

| Trading Hours |

Monday to Thursday:

Session I: 08.45– 12.00 Session II: 13.30 – 16.15 Friday:

Session I: 08.45 - 11:30 Session II: 14.00 – 16.15 |

| Settlement | Cash, T + 1 |

The Benefits of IDX LQ45 Futures

The Benefits of IDX LQ45 Futures are :

IDX30 Futures

Futures is a contracts to buy or sell an underlying (can be index, stock, bond, etc.) at a certain price in the future. Index Futures are futures contracts that use stock indices as their underlying.

IDX30 Futures is an agreement requiring parties to buy or sell a certain number of Underlying in the form of Index at a certain price in certain period of time. IDX30 Futures use IDX30 index as their underlying. The IDX30 index is an index of 30 stocks that have been selected from the LQ45 index. Thus, IDX30 are the index consist the most 30 liquid stock in IDX. The following are specifications of IDX30 Futures;

| Criteria | Specification |

|---|---|

| Contract Code | IDX30MY |

| Underlying | IDX30 Index |

| Multiplier | IDR 100.000 |

| Tick Size | 0,1 Point Index |

| Contract Months | 1 Month, 2 Months dan 3 Months |

| Initial Margin | 4% x Index point x Number of contract x Multiplier |

| Post-Order Initial Margin | Stadardized Portfolio Analysis of Risk (SPAN) ® |

| Auto Rejection | 10% |

| Trading Hours |

Monday to Thursday:

Session I: 08.45– 12.00 Session II: 13.30 – 16.15 Friday:

Session I: 08.45 - 11:30 Session II: 14.00 – 16.15 |

| Settlement | Cash, T+1 |

IDX30 Futures Code

Code:IDX30MY

M : Month of Expiry

Y : Year of Expiry (last number)

Contract Months Code| Month | Month Code |

|---|---|

| January | F |

| February | G |

| March | H |

| April | J |

| May | K |

| June | M |

| July | N |

| August | Q |

| September | U |

| October | V |

| November | X |

| December | Z |

IDX30G0

IDX30 Futures expiry in February 2020

Watch video of IDX30 Futrues

KBIA MSLCHK Futures

A Foreign Index Futures Contract (KBIA) is a contract to buy or sell an underlying index listed on a foreign exchange at a specific price and time in the future. This product allows investors to gain exposure to the movements of foreign stock indices.

The MSLCHK Futures is based on the MSCI Hong Kong Listed Large Cap Index (Bloomberg Ticker: MXHKLU), representing the movement of large-cap stocks listed on the Hong Kong Stock Exchange.

The specifications for MSLCHK Futures are:

|

Kriteria |

Spesifikasi |

|

Stock Code |

MSLCHKMY |

|

Underlying |

MSCI Hong Kong Listed Large Cap Index (Bloomberg Ticker: MXHKLU) |

|

Multiplier |

Rp10,000 |

|

Tick Size |

1 index point |

|

Contract Period |

1, 2, and 3 months |

|

Initial Margin |

3% x Index Value x Number of Contracts x Multiplier |

|

Post-Order Initial Margin |

Standardized Portfolio Analysis of Risk (SPAN) ® |

|

Auto Rejection |

15% |

|

Trading Hours |

Monday to Thursday: |

|

Settlement |

Cash, T+1 |

Indonesia Government Bond Futures

Indonesia Government Bond Futures (IGBF) contract is an agreement that requiring parties to buy or sell a number of Indonesia Government Bond at a price and within a certain period of time in the future As of January 2017, based on Report Stated in DJPPR report, Total Government Bond in Indonesia Rp1.554,92 Trillion. Outstanding of SUN Seri Benchmark Rp.167,87 Trillion, where 62% dominated by SUN Seri Benchmark 5 and 10 years. With huge amount of outstanding, Indonesia significantly need hedging instruments for Government Bond Market. This include Issuers as well as Investors / Primary Dealers.

The specification of IGBF :

| IGBF | ||

|---|---|---|

| Product | 5-Year Benchmark Indonesia Government Bond Futures | 10-Year Benchmark Indonesia Government Bond Futures |

| Instrument Code | BM05H6 | BM10H6 |

| Contract Size | IDR 1,000,000,000 | IDR 1,000,000,000 |

| Quotation | Price | Price |

| Tick Size | 0.01 (1 bp) | 0.01 (1 bp) |

| Tick Value | IDR 100,000 | IDR 100,000 |

| Auto Rejection | 300bp from reff price | 300bp from reff price |

| Initial Margin | 1% X Contract Size X Number of Contract X Futures Price | 2% X Contract Size X Number of Contract X Futures Price |

| Trading Hours |

Monday to Thursday:

Session I: 08.45– 12.00 Session II: 13.30 – 16.15 Friday:

Session I: 08.45 - 11:30 Session II: 14.00 – 16.15 |

Monday to Thursday:

Session I: 08.45 – 12.00 Session II: 13.30 – 16.15 Friday:

Session I: 08.45 - 11:30 Session II: 14.00 – 16.15 |

| Contract Month | 3 months in the March quarterly cycle (March, June, September and/or December) | 3 months in the March quarterly cycle (March, June, September and/or December) |

| Settlement | Cash Settlement (T + 1) | Cash Settlement (T + 1) |

| Liquidity Provider | Yes | Yes |

| Spread LP | 55 bp (±0.55%) | 70 bp (±0.70%) |

| Min Quantity | 10 contracts | 10 contracts |

Why do we need IGBF?

-

High interest rates may threaten the sustainability of fiscal policy: IGBF could be seen as equilibrium interest rates for DMO to do fiscal activity

-

Broadening Investor Base

-

IGBF will attract new investor base due to hedging purpose / necessity to have physical bond

-

Broader investor base will reduce reliance on a captive market

-

Improve liquidity due to additional quantity of investor with diverse risk profiles

-

- Cash and Futures markets are closely related.

Secondary Market

Enhancing Liquidity

-

Increase hedging activity and promote risk management practice.

-

Cash and Futures market are closely linked.

Basket Bond Futures

Basket Bond Futures (BBF) is an agreement between parties to buy or sell a set of Government Bond at a certain price and within a certain time in the future.

Considering the current development of the debt securities market in Indonesia and the large outstanding value, particularly in government bond securities, a hedging instrument is needed for its Market. This includes Investors or Primary Dealers.

BBF business specifications:

| Criteria | Basket Bond Future |

|

|---|---|---|

| 5 Years | 10 Years | |

| Underlying | Government Bond with maturities of 4 to less than 7 years | Government Bond with maturities of 7 to less than 11 years |

| Code | GB05MY | GB10MY |

| Multiplier | Rp1.000.000.000,- | |

| Tick Size | 1 bp (0,01%) | |

| Auto Rejection | 600 bp | |

| Contract Month | March, June, September, or December | |

| Pre-Order Intial Margin | 1% * IGBF Price * Number of Contract * Multiplier | 2% * IGBF Price * Number of Contract * Multiplier |

| Fee | ||

| BEI | Rp10.000/contract | |

| KPEI | Rp6.000/contract (60% dari IDX fee) | |

| Guarantee Fund | 0,0003% of Transaction Value | |

Why do we need BBF?

- Hedging instrument for Government Bond Portfolio.

- Can be used for profit management in bullish and bearish market.

- Broadening Investor Base

- BBF will attract new investor base due to hedging purpose.

- Improve liquidity due to additional quantity of investor with diverse risk profiles.